1. Can you pay family at all?

Yes. CRA does not ban paying family members just because they are related to you. Ontario small business owners put spouses, kids, and parents on the books all the time.

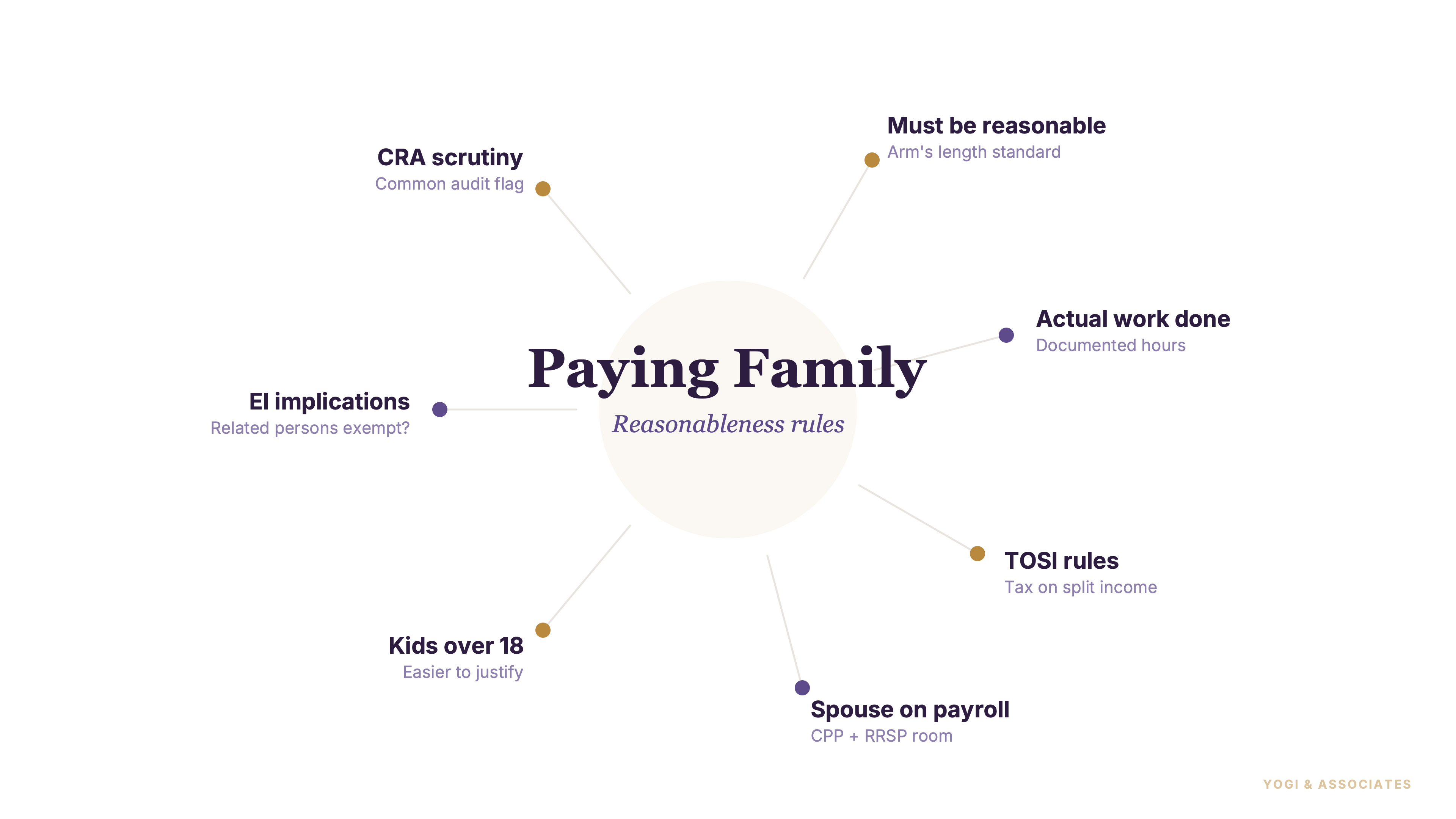

But non-arm's length is the tax term for related people like a spouse, child, parent, or sibling. That label matters because CRA will look harder at these payments than it would with an unrelated employee.

So the real question is not whether you can do it. The real question is whether the work is real, the pay is fair, and the paperwork proves both.

2. CRA reasonableness test

CRA's test is pretty plain. The salary has to be reasonable when you consider the person's age, the work they actually do, and what you would pay someone else for the same job.

That is especially important with children and spouses. owners usually get into trouble when they decide the number first and invent the role after.

But if the work is real and the pay looks like market pay, the deduction can hold up. Our small business deductions guide is useful once you start separating legitimate payroll from wishful thinking.

3. Payroll, T4, EI, and CPP

Family employees are not off in a special side category for payroll. CRA says salaries paid to children and a spouse or common-law partner are reported on T4 slips the same way you would report other employees.

CPP also applies normally because the CPP rules do not carve out family employees from pensionable employment. We've found that owners often remember salary and forget the payroll follow-through that comes with it.

EI is the one area where things can change. But related employees may not be in insurable employment unless the contract looks substantially similar to what you would have agreed to with an arm's-length employee, and CRA can issue a ruling if you are not sure.

4. Records that keep it deductible

CRA wants records, not stories. And the line CRA uses is blunt: keep documents to support the salary you pay your child, and use the same rules for a spouse or common-law partner.

That means job descriptions, timesheets, and proof of payment. Cheque or direct deposit is cleaner than cash, even though CRA says if you pay cash you should have the child sign a receipt.

So treat the family member like any other employee from day one. Our self-employed taxes and T2125 guide is helpful if you are still moving from informal owner draws into proper payroll habits.

5. Paying minor children

Paying a minor child is allowed, but it gets extra scrutiny. CRA specifically says the salary has to be reasonable when you consider the child's age and what you would pay someone else.

So age-appropriate work matters. filing, social media help, simple admin, and cleaning up inventory records are easier to defend than a made-up management title.

And the records need to be just as good as the records for any adult employee. If the child did not really do the work, the deduction is weak no matter how nice the spreadsheet looks.

6. TOSI and family dividends

TOSI means Tax on Split Income — the rule that can tax certain amounts paid to family members at the highest marginal tax rate. And starting with the 2018 tax year, those updated rules began applying to adults age 18 or older.

That changed the old dividend-planning math in a big way. This is why so many owners still repeat advice that worked years ago but no longer works cleanly.

The most common exclusion is the excluded business test, where the family member was actively engaged on a regular, continuous, and substantial basis. CRA says that test is deemed met if the person worked an average of 20 hours per week in the business during the year, or met that threshold in any 5 prior years.

7. What still works after TOSI

TOSI did not kill every family-planning idea. But it did make lazy dividend splitting a much worse bet unless an exclusion like excluded business, excluded shares, or a reasonable return actually fits the facts.

For adults age 25 or older, excluded shares and reasonable return can still matter. that analysis belongs beside your incorporation and compensation planning, not as an afterthought when year-end is already here.

So if dividends are on the table, read our salary vs dividends guide and our T2 corporate tax return guide next. And if you want a simple income-splitting tool that still exists outside TOSI, CRA still says a spousal RRSP can help split retirement income more evenly between spouses.

Paying family can be perfectly valid, but only when the payroll, records, and tax logic all line up. If you want that reviewed before CRA does, we can help.

Book a Free Consultation