1. The short version of the tradeoff

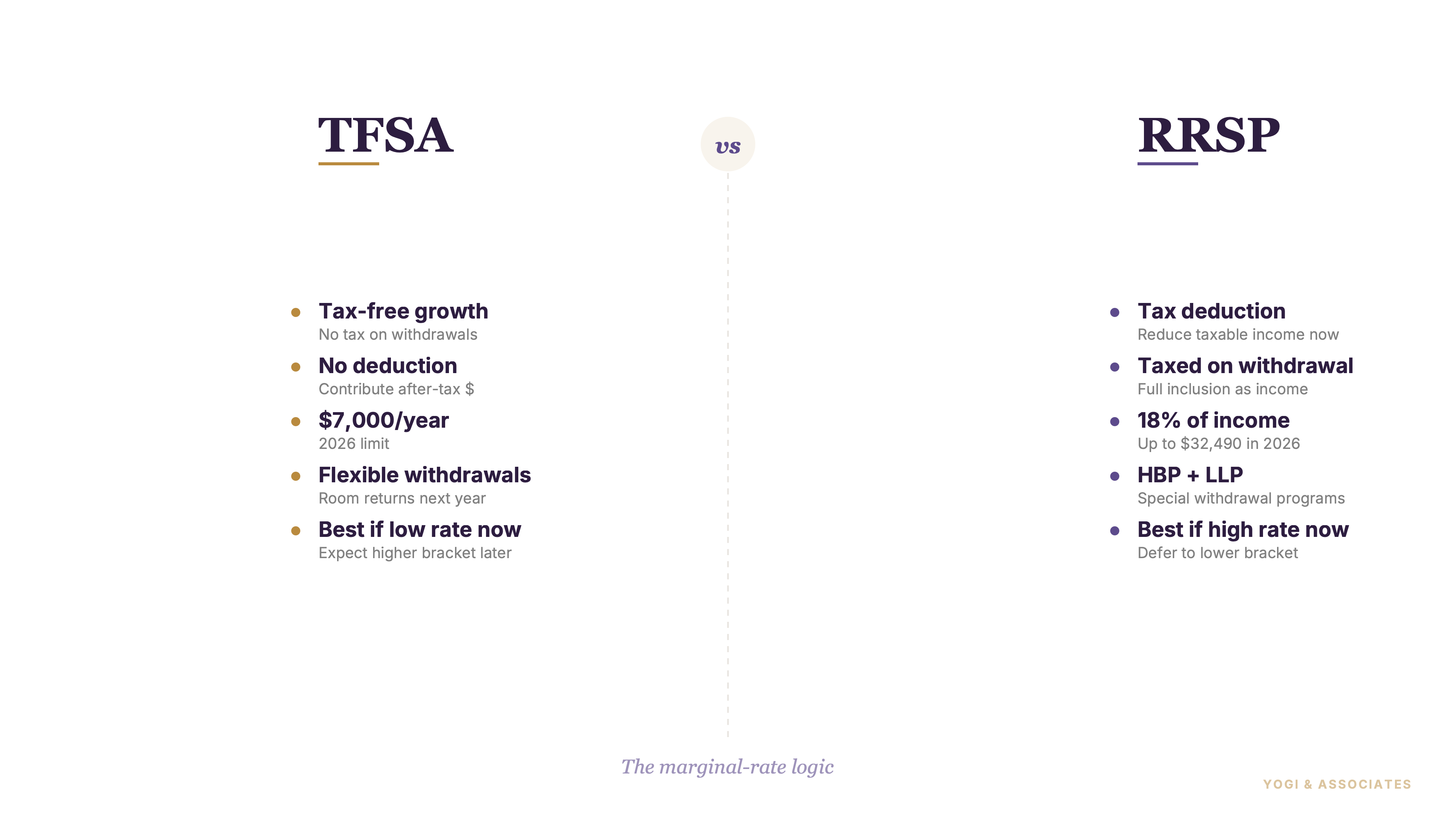

For Ontario taxpayers, the RRSP vs TFSA decision comes down to marginal rates now versus later. RRSPs work on a simple idea. You get a deduction now, the money grows sheltered, and you're taxed when you withdraw it later. The bet is that your tax rate in retirement will be lower than your tax rate today.

TFSAs work on the opposite idea. You use after-tax dollars with no deduction up front. But the growth and every withdrawal after that are tax-free — forever.

most people treat these two accounts like they're interchangeable. They're not — one is a tax deferral, the other is a tax exemption. Those are very different deals, and they reward very different life stages.

2. TFSA basics and 2026 limits

The TFSA dollar limit for 2026 is $7,000. That's the new room added on January 1. If you've been eligible since the program started in 2009 and never contributed a dollar, your cumulative room in 2026 is $109,000.

Contributions aren't deductible. But investment growth inside the TFSA — interest, dividends, capital gains — is never taxed. Withdrawals aren't taxed either, and the amount you take out is added back to your contribution room the following calendar year.

The TFSA is the single most underused account in Canada. Too many people use it as a chequing account with a fancy name, parking cash at 2% interest and missing the whole point — which is sheltering growth. A TFSA holding long-term investments is where the real tax saving happens.

3. RRSP basics and 2026 limits

Your 2026 RRSP room is the lower of two numbers: 18% of your 2025 earned income, or the annual dollar cap of $33,810. The dollar cap only kicks in if your 2025 earned income was roughly $187,833 or more.

Contributions are deductible against your income in the year you claim them. That's the headline benefit. Every dollar you put in reduces your taxable income and triggers a refund based on your marginal rate — the rate on your next dollar of income.

But here's the piece people miss. When you eventually pull money out of the RRSP in retirement, it's fully taxed as income — so the RRSP isn't free money, it's a tax deferral, and the math only works if your retirement marginal rate is lower than today's. We see clients forget this constantly, especially people who stay high-income into their 60s.

4. The marginal rate decides it

Here's the rule we use with clients. If your marginal rate today is higher than your expected marginal rate in retirement, lean RRSP. If it's lower, lean TFSA.

A 26-year-old making $55,000 in Ontario is in roughly the mid-20s marginal bracket. If they expect to earn more later and retire at a similar or higher income, their RRSP deduction today isn't buying much. The TFSA is usually the better move.

A 42-year-old making $140,000 is a different story — they're hitting a mid-40s marginal rate. An RRSP contribution gives back a big refund now, and they're very likely to retire at a lower income. this is where the RRSP quietly wins.

Check Ontario's current brackets in our 2026 Ontario tax brackets breakdown before you run the math yourself. And if you're paying yourself from a corporation, the decision gets even more layered — we cover that in salary vs dividends in Ontario.

5. HBP and LLP — RRSP's side doors

The RRSP has two escape hatches that often get overlooked. Both let you pull money out without paying tax — as long as you pay it back.

The Home Buyers' Plan (HBP) lets first-time buyers withdraw up to $60,000 from their RRSP to buy or build a home — a ceiling that was raised from $35,000 back in April 2024. A couple can pool up to $120,000 toward the same purchase. You have 15 years to repay, with a grace period before repayments start.

The Lifelong Learning Plan (LLP) lets you pull up to $10,000 per year from your RRSP to fund full-time training or education, with a lifetime cap of $20,000. It covers you or your spouse — but not your kids. Repayments run over 10 years.

So the RRSP isn't as locked-up as people assume. That's a big deal for anyone worried about tying up cash for 30 years — you don't have to. You just have to know the rules.

6. A quick note on the FHSA

There's a third account worth mentioning: the First Home Savings Account. It's designed for first-time home buyers and it has the best of both worlds — RRSP-style deduction going in, TFSA-style tax-free growth coming out.

If you qualify and you're saving for a first home, the FHSA almost always beats using the HBP alone. You can also stack it with the HBP for the same purchase.

first-time buyers should fill the FHSA first, then the TFSA, then think about HBP withdrawals. We'll break that full stack down in a dedicated FHSA post — this one is about the core TFSA vs RRSP call.

7. How we tell clients to choose

No single rule works for everyone, but we see patterns. Here's the short version of how we talk it through with people in the office:

- Low income year (under ~$55K). Use the TFSA first. Your RRSP deduction would be worth almost nothing right now — save the deduction for a future high-income year.

- Mid income ($55K–$100K). Usually a split. Enough RRSP to claw back the tax owing, TFSA for everything else.

- High income ($100K+). RRSP first, then TFSA. The deduction is finally worth real money, and you're likely retiring at a lower rate.

- Saving for a first home. FHSA, then TFSA, then HBP withdrawal if you need more.

- Short-term savings goal. TFSA. Always. You don't want to trigger an RRSP withdrawal tax hit for a two-year goal.

And here's the sentence we repeat the most: don't pick one and forget it. The right account changes as your income changes, and the smartest thing most people can do is revisit this question every couple of years.

If you want help running the actual numbers for your situation, check out our personal tax service. We put this together in the context of our broader Canadian tax preparation guide if you want the full picture.

Stuck on whether to feed the TFSA or the RRSP this year? We run the marginal rate math for clients all the time. Let's look at your numbers together.

Book a Free Consultation