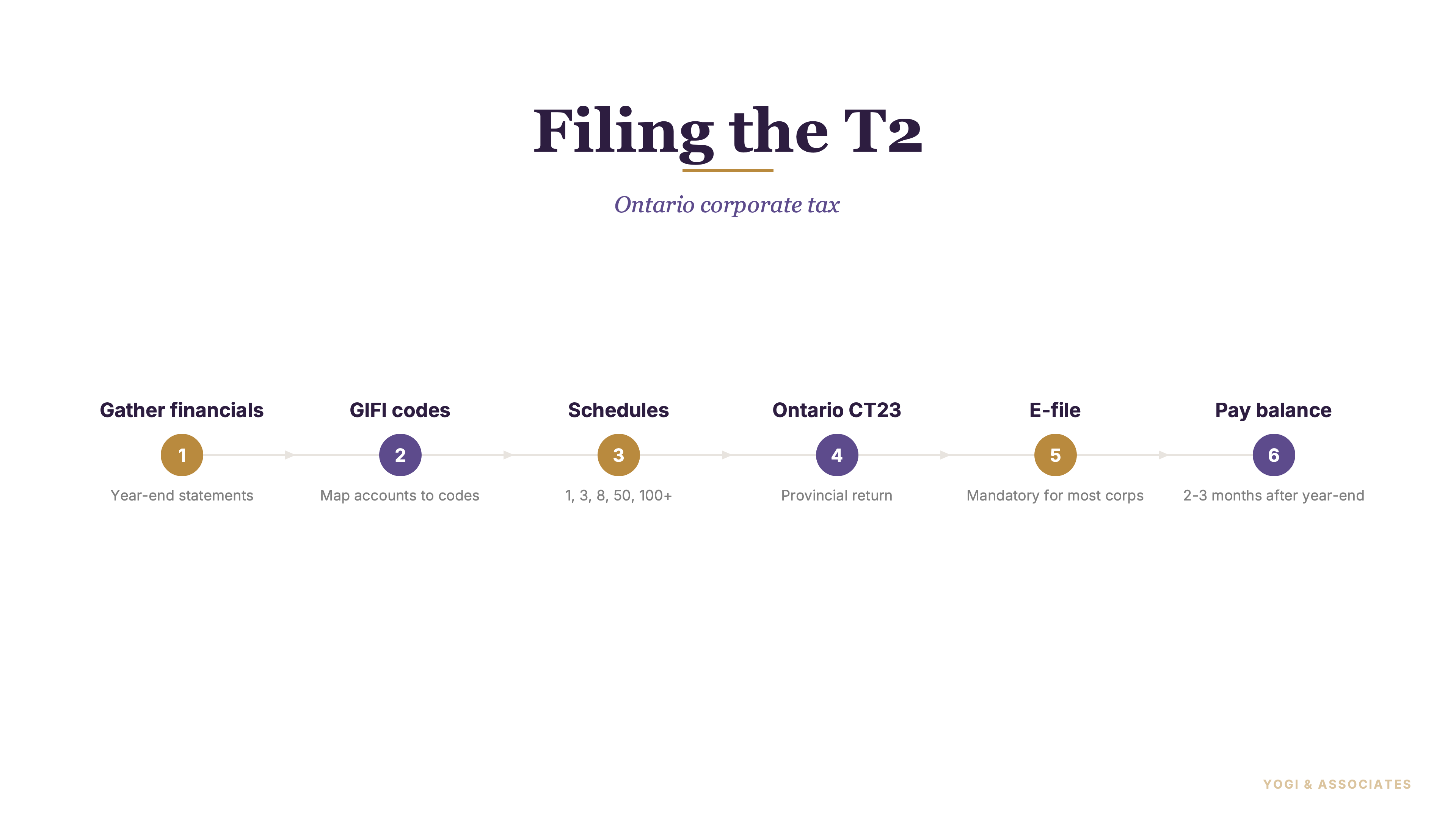

1. What the T2 actually is

The T2 is the corporate version of a T1 — one return per corporation, per tax year. Every resident corporation files it, whether active, dormant, profitable, or losing money. Doesn't matter.

The return itself is a summary page. The real work lives in the schedules attached to it, and those schedules walk your financial statements into the tax calculation.

the owners who struggle with their first T2 aren't struggling with the form. They're struggling because the bookkeeping for the year was never properly closed. Garbage in, garbage out.

2. Filing and payment deadlines

Here's the part most first-time filers get backwards. Filing and paying are two different deadlines. Paying comes first.

The T2 return itself is due six months after the end of your fiscal year. So a December 31, 2025 year-end means the T2 is due June 30, 2026. An August 31 year-end means February 28 — simple rule.

But the tax itself is due earlier. The balance of tax is due two months after year-end for most corporations. If you're a Canadian-controlled private corporation (CCPC) that claimed the small business deduction (SBD) and meets the CRA's income thresholds, you get an extra month — so your balance is due three months after year-end.

We see this catch people every year. They file on time in month six and think they're fine, but arrears interest has been running since month two or three. The filing deadline is not the payment deadline.

- T2 return filing: 6 months after fiscal year-end.

- Tax payment, most corporations: 2 months after fiscal year-end.

- Tax payment, eligible CCPCs claiming SBD: 3 months after fiscal year-end.

3. Mandatory e-file (yes, everyone)

You used to be able to paper-file a T2 if your gross revenue was under $1 million. Not anymore. Bill C-47 killed that threshold for tax years beginning after 2023.

So as of 2024 and onward, basically every Canadian corporation must file its T2 electronically. If you paper-file when you were required to e-file, CRA charges a flat $100 penalty per return. It's a cheap mistake to avoid.

Plus, e-filing gives you a confirmation number on submission. Paper returns can sit in processing limbo for months. The electronic route is the only sane way to file now — even the rare corporations that could still paper-file probably shouldn't.

4. The schedules you'll actually touch

A full T2 has dozens of schedules. Most small Ontario corporations only need a handful. These are the ones we fill out on nearly every file:

- Schedule 1 — Net Income for Tax Purposes. This is the income reconciliation. You start with your accounting net income and add back or subtract items the CRA treats differently (non-deductible meals, amortization, and so on). It's how your books become tax numbers.

- Schedule 8 — CCA (Capital Cost Allowance). The tax version of depreciation. You group your fixed assets into classes with set rates, and this schedule calculates the annual deduction. Vehicles, computers, buildings, tools — they all live here.

- Schedule 50 — Shareholder Information. If you're a private corporation, you list any shareholder who owns 10% or more of any class of shares. Up to the top 10 shareholders.

- Schedule 100 — Balance Sheet (GIFI). Your year-end balance sheet, translated into CRA's standardized codes. Assets, liabilities, equity.

- Schedule 125 — Income Statement (GIFI). Your income statement, same idea. Revenue and expenses by GIFI code.

And depending on your situation, you may also touch Schedule 3 (dividends received), Schedule 7 (aggregate investment income), Schedule 11 (shareholder transactions), Schedule 23 (associated corporations), and a provincial schedule for Ontario. We flag the relevant ones during the file review.

5. GIFI — the part that trips people up

GIFI stands for General Index of Financial Information — the CRA's standardized chart of accounts that maps your books to T2 schedules. Every line on your financial statements gets a four-digit GIFI code.

So "Office Supplies" in your bookkeeping becomes GIFI 8811. "Cash" becomes 1001. It's how CRA can read balance sheets and income statements from millions of different corporations in one consistent format.

Honestly? GIFI coding is the quiet boss of the T2. If your chart of accounts is messy, the GIFI mapping is a nightmare.

If your bookkeeping is clean, the GIFI mapping is automatic in every professional tax program. This is why we push clients to invest in proper bookkeeping before chasing a tax optimization.

6. Ontario rates for 2026

Here's where 2026 gets interesting. Ontario's combined corporate tax picture has two layers — federal plus provincial — and the small business rate is changing mid-year.

For a CCPC claiming the small business deduction on the first $500,000 of active business income, the combined federal and Ontario rate is roughly 12.2% (9% federal + 3.2% Ontario). Above $500,000, the combined general rate is roughly 26.5% (15% federal + 11.5% Ontario).

But the 2026 Ontario Budget announced a cut to the provincial small business rate from 3.2% to 2.2%, effective July 1, 2026. If your fiscal year straddles that date, the rate gets pro-rated for the days on each side. So a December 31, 2026 year-end corporation claiming the SBD will see a blended Ontario rate for the year. Run your own numbers with the Ontario corporate tax calculator — it handles the SBD, general rate, and the July 1 pro-ration automatically.

this is exactly the kind of change that gets missed when owners self-file. If you want more on how the Ontario provincial side fits together, our Ontario tax brackets 2026 explainer walks through the personal side, and our salary vs dividends guide covers how rate changes ripple into owner compensation planning.

7. Where first-time filers go wrong

We see the same cluster of mistakes every spring. None of them are about the math on the T2 form itself:

- Confusing the filing and payment deadlines. Paying at month six is late. Interest has been running since month two or three.

- Messy bookkeeping. Shareholder loan accounts that were never reconciled, HST cleared to the wrong GL, expenses coded to "Other" with no detail.

- Missing CCA on new assets. You bought a vehicle or computer and just expensed it. That's not how it works — it belongs on Schedule 8.

- Forgetting the 15-month shareholder loan rule. Loans to owners must be repaid within one year after the corporation's year-end, or they become taxable income. See the shareholder loan rule.

- Claiming 100% of meals. Only 50% is deductible. The add-back goes on Schedule 1.

- Missing deductions on the expense side. Our small business tax deductions guide covers the ones owners most often leave on the table.

And one more: waiting until May or June to start. A December year-end corporation should have books closed by February, first draft T2 by March, filed and paid by the end of April. Comfortable, not cramming.

8. A clean filing workflow

Here's the order we use on every T2 engagement. Steal it:

- Close the books. Reconcile bank, credit cards, HST, payroll liabilities, shareholder loan. Nothing goes forward until these tie.

- Adjust for tax. Book year-end entries — depreciation, accruals, prepaid, inventory adjustment.

- Map to GIFI. Verify every GL account has a sensible GIFI code. Fix any "catch-all" accounts first.

- Draft Schedule 1. Start with accounting net income, add back non-deductibles, subtract tax-only deductions, land at net income for tax.

- Run CCA on Schedule 8. Add new acquisitions, calculate half-year rule, dispose of anything sold.

- Fill Schedule 50. Shareholders at 10% or more of any class.

- Populate GIFI Schedules 100 and 125. Balance sheet and income statement in GIFI format.

- Calculate tax and pay it. Do this before the payment deadline (month 2 or 3), not the filing deadline (month 6).

- E-file the return. Save the confirmation number.

This whole process is much cleaner when the bookkeeping is handled throughout the year instead of reconstructed the week before filing. That's what our corporate tax service is built around — closing the year as it ends, not in a panic six months later.

Worried about something the CRA might already be looking at? We also handle CRA audit support for T2, HST, and payroll files. And for the broader picture, our Canadian tax preparation pillar guide ties T2 into the rest of the year's filings.

First T2 coming up and not sure where to start? We handle the whole thing — books, schedules, GIFI, e-file, payment calculation. One call and you'll know exactly what it costs and when it's due.

Book a Free Consultation