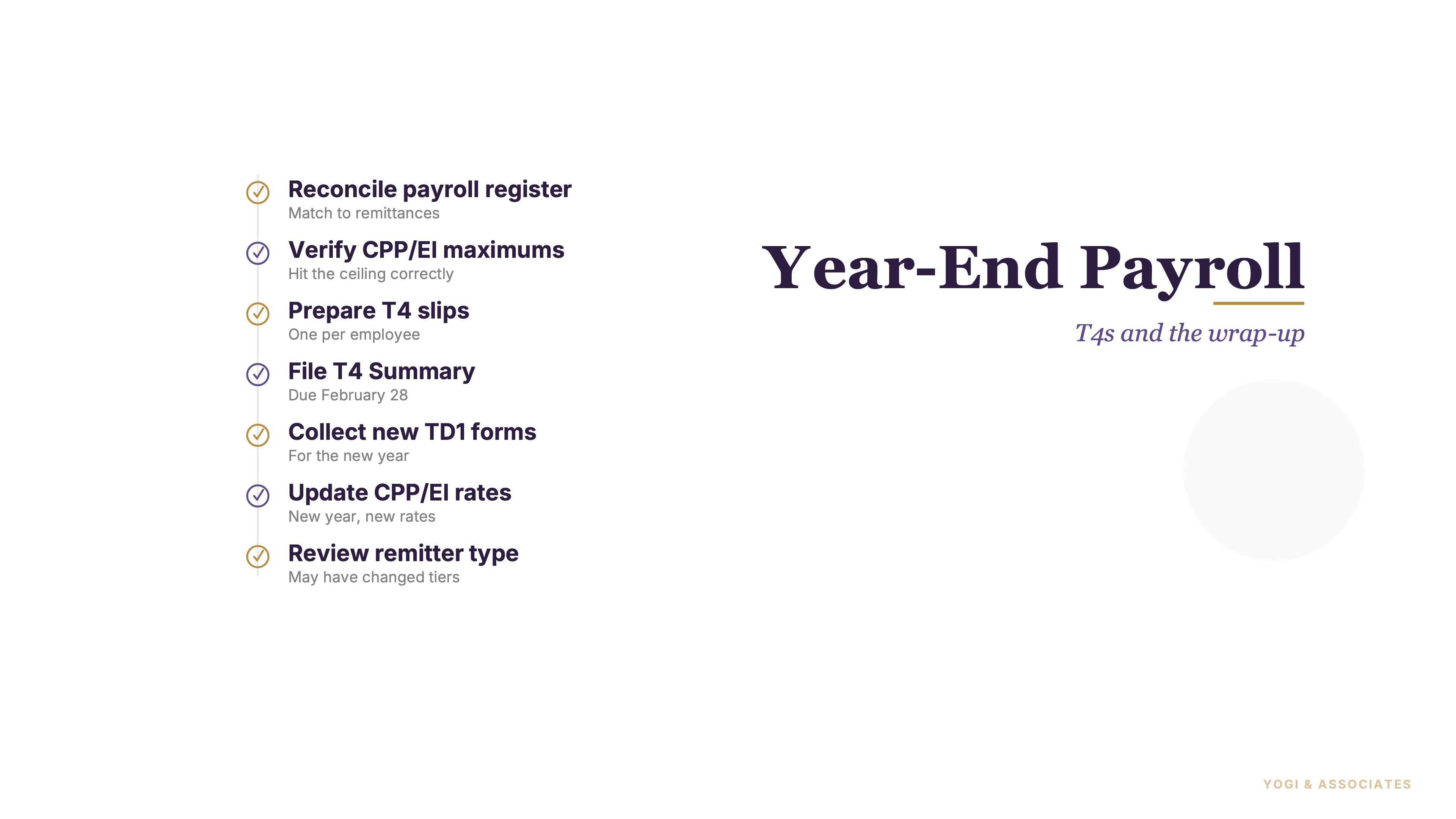

1. Reconcile payroll before you touch the slips

The best year-end payroll checklist starts before slip prep. You should reconcile year-to-date employee totals to the general ledger first, because every later step depends on that base being right.

Match gross wages, CPP, EI, income tax, employer payroll costs, and remittances to the books. But do not stop at totals. If one employee file is off, the grand total can still look fine while the slips are wrong.

So pair this with our Canadian payroll guide and our year-end bookkeeping checklist. In our view, payroll close and year-end books should be checked together, not in separate silos.

2. T4 season is the anchor deadline

The federal year-end payroll deadline most employers care about is simple. T4 slips and the T4 Summary are due on or before the last day of February following the calendar year.

That date drives the whole close calendar. Employers should work backward from it, not forward from January with vague optimism.

So if T4 prep is the weak point in your process, our T4 guide is the best companion piece here. And our 2026 tax deadlines post helps keep the wider filing calendar visible.

3. Check the other slips people forget

Employers often close payroll and only think about T4 slips. But year-end payroll can involve other slips too.

T4A (the slip you issue to non-employees you've paid for services — the subcontractor and freelance equivalent of a T4) matters when service payments exceed $500 in a calendar year. And if you have a place of business in Quebec, CRA says you may also have to file RL slips with Revenu Québec, including RL-1 for employment income.

This is one of the easiest year-end misses for small employers. So review your contractor ledger and your Quebec payroll files before assuming the job is just federal T4s.

4. Run a math check before CRA does

CRA has its own payroll math review called PIER. PIER (Pensionable and Insurable Earnings Review — CRA's pre-check that flags math errors on your T4 slips before processing them) looks for mismatches between the deductions you reported and the amounts CRA calculates from the earnings you reported.

If CRA finds a discrepancy, it can send a PIER notice asking you to correct the file. Employers should do that review themselves first, especially on CPP, EI, and insurable earnings logic.

But if you discover you over-deducted CPP or EI, there is also a cleanup tool. Form PD24 can be used to ask CRA for a refund of overpaid CPP or EI. In our view, catching that before the notices start is always the better route.

5. Clean up employee records for the new year

Year-end is the right time to review employee setup, not just payroll totals. That includes names, SINs, addresses, province of employment, and tax-credit forms.

CRA requires a federal TD1 and a provincial or territorial TD1 when someone starts employment, and a new form when their personal tax credit amounts change. A new-year review is smart even when nothing obvious changed, because stale employee master data creates dumb slip errors.

So ask who moved, who changed provinces, who changed claim amounts, and who still has an old form on file. In our view, this is one of the cheapest year-end control steps you can add.

6. Update rates and pension reporting for January 1

January 1 is not just a calendar flip. CRA updates CPP contribution rates and maximums each January 1, and it also updates EI premium rates and the Maximum Insurable Earnings each January 1.

That means the payroll system needs fresh settings before the first payroll of the new year. And if employees are in an RPP or DPSP, box 52 on the T4 has to report the pension adjustment, which reduces the employee's RRSP deduction limit for the next year.

This is the part employers forget when they say "year-end is done." But if January settings are wrong, the next year starts broken on day one.

7. Clear year-end terminations and final payroll loose ends

Year-end terminations need more than a final pay run. If someone had an interruption of earnings near year-end, the ROE has to be handled on the normal ROE schedule.

CRA and Service Canada guidance still point to the same basic timing rules: paper ROEs are due within 5 calendar days after the interruption of earnings or when the employer becomes aware of it, and electronic ROEs generally follow the pay-period-end rule. This is why year-end offboarding should be reviewed separately from T4 prep.

So if someone left in December or early January, check the ROE before you call payroll close complete. And if payroll year-end already feels too heavy, our payroll service can take that work off your plate.

Year-end payroll is manageable when the file stays clean all year. If you want help closing payroll properly and avoiding February panic, we can help.

Book a Free Consultation