1. What the Quick Method actually changes

The Quick Method changes how you calculate what goes back to CRA. It doesn't change the tax rate your customer sees on the invoice.

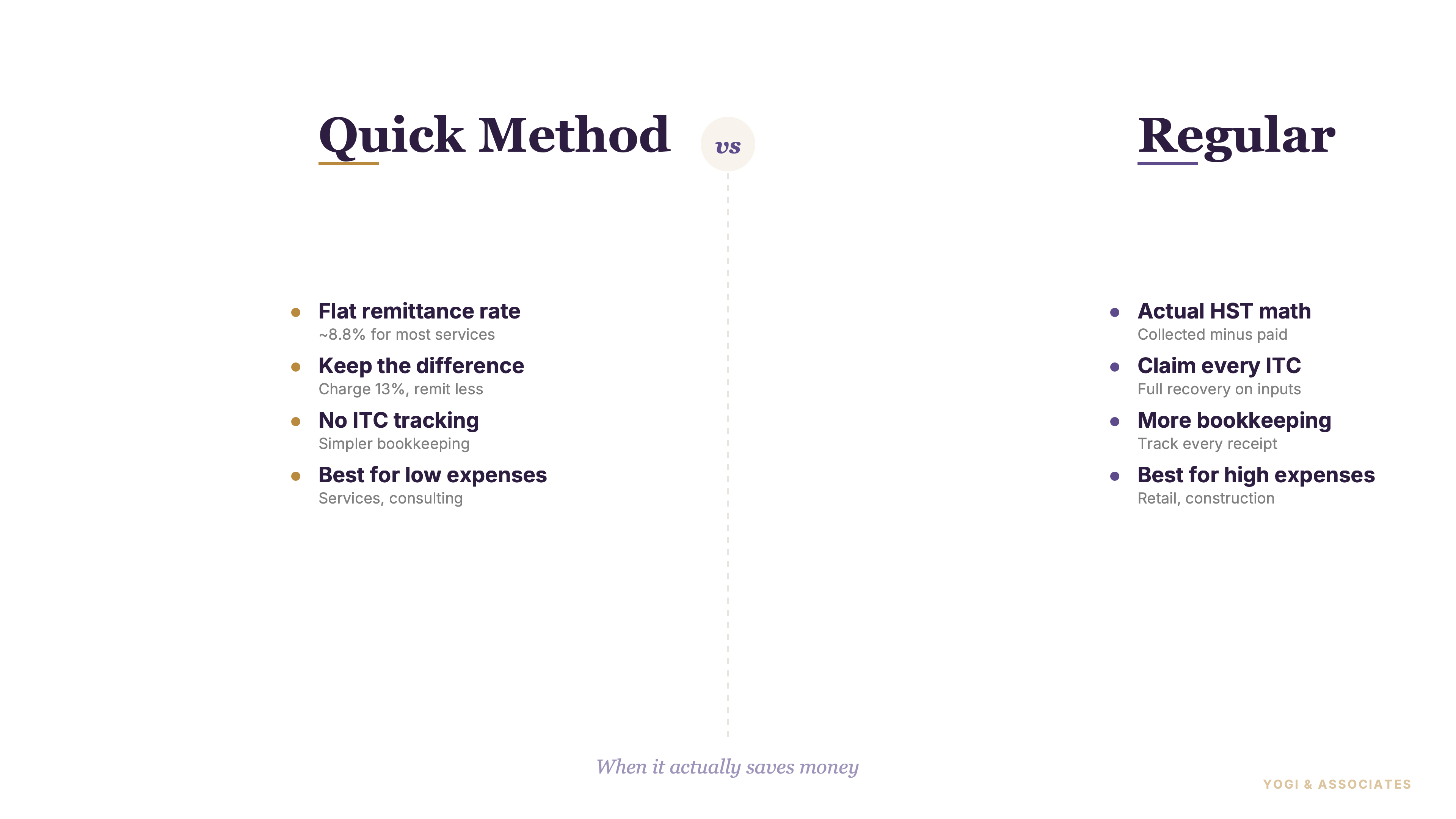

You still charge GST at 5% or HST at the applicable provincial rate. But you remit only a portion of that tax — a published remittance rate that's always lower than what you charged. The spread between the two is the savings.

This is why the method gets misunderstood as a “trick.” It isn't — it's a legal trade. You give up operating ITCs; in exchange, CRA lets you remit less than you collected. Our GST/HST guide is the better place to start if you want the full system around it.

2. Who can use it and who cannot

The headline rule is the $400,000 cap. Annual worldwide taxable supplies, including zero-rated supplies and those of associates, must stay at or below $400,000 under CRA's recent-quarter tests.

Eligibility isn't just about revenue, though. The exclusion list matters more, because many owners hear “small business” and assume automatic eligibility. It isn't automatic. CRA specifically excludes: bookkeeping, financial consulting, tax consulting, tax return preparation, legal, accounting, and actuarial services, plus listed financial institutions, charities, and several public bodies.

Full disclosure: Y&A is on that excluded list. Accounting firms like ours can't use the Quick Method on our own invoices — neither can bookkeepers, lawyers, or financial consultants. But we run the math on it for eligible clients every month, which means we've seen the exact shape of the win and the exact shape of the loss. Excluded by rule doesn't mean unfamiliar.

A lot of classic office-based service businesses qualify — solo consultants, cleaners, photographers, writers, designers, contractors without heavy material costs. A lot of regulated advice businesses don't.

3. How the remittance math works

The rate depends on your business type (service vs. retail/purchase-heavy), where the supply is made, and where your permanent establishment is located. The method is simple. The table choice is not.

For a service business in Ontario supplying HST at 13%, the remittance rate is 8.8%. Your customer still pays the full 13% HST on the invoice. You remit 8.8% of the HST-included total to CRA. The spread goes to your business as a direct saving — roughly 4.2% of gross receipts on every qualifying sale.

Test this part carefully. If you're a solo operator or contractor, our freelancer HST guide helps frame the math in real life.

4. ITCs, capital assets, and the 1% credit

Under the Quick Method, you generally can't claim ITCs on operating expenses. The lower remittance rate is the trade — it's supposed to stand in for the operating ITCs you're giving up.

You can still claim ITCs on certain capital items: real property, and capital assets such as computers and vehicles. CRA also gives a 1% credit on the first $30,000 of eligible supplies (including GST/HST) in each fiscal year, as long as the election qualifies from the start of that year.

This is where the regular method sometimes wins. If your business has meaningful taxable operating purchases — inventory, materials, contractor subcontracts — the ITCs you'd claim under the regular method can beat the Quick Method spread. Our ITC guide shows the contrast.

5. How to elect with GST74

CRA calls this an election — a formal choice to use a different tax treatment than the default, filed once and effective for a fiscal period. You can elect online through My Business Account or Represent a Client, or file Form GST74 on paper.

The effective date has to be the first day of a GST/HST reporting period. You must also have been in business throughout the 365-day period ending immediately before your current reporting period — unless you're a new registrant, in which case different rules apply.

This isn't a form to backdate in your head. Our CRA filing guide helps if you're already working inside the portal.

6. When the Quick Method actually saves money

The Quick Method wins for service businesses with low overhead. It loses for businesses with heavy taxable purchases that would otherwise create strong ITCs. Here's the rough shape of the decision:

- Solo consultant, coach, freelance designer, copywriter: almost always wins. Low overhead, lean ITCs, the 4.2% spread is pure gain.

- Cleaner, photographer (light gear years), small service business: usually wins. Test both methods if equipment purchases are pending.

- Photographer (heavy gear year), contractor buying materials: depends on the year. Test both methods before electing.

- Retailer, trades with material costs, restaurants, anyone with heavy taxable inputs: regular method usually wins. ITCs on inventory and materials beat the spread.

- Accountant, bookkeeper, lawyer, financial consultant, actuary: not eligible. Excluded by rule.

A typical Ontario service business charges 13% HST and remits 8.8%. If operating costs are lean, the 4.2% spread beats the operating ITCs you'd otherwise claim. Once purchases get chunkier, the regular method catches up fast. That's why the savings story is real for consultants and cleaners, but weak for businesses buying serious taxable inputs.

7. A clean way to decide before you file

Start with a short checklist. First, confirm you're under the $400,000 cap and not in an excluded profession (see section 2).

Second, compare the value of your lost operating ITCs against the lower remittance rate plus the 1% credit on the first $30,000 of eligible sales. Third, check the election timing — a revoked election triggers at least a one-year wait before you can elect again, so the decision isn't casually reversible.

Most owners should run both methods once before deciding. Plug your numbers into the Ontario HST calculator — it shows exactly how much you'd keep on Quick vs. remit under the standard method. If you want that done cleanly, our HST filing service is the faster route.

Not sure whether the Quick Method would actually save money for your specific business? We run both methods side-by-side for GTA owners before they elect — so you're not guessing based on a blog post. We won't recommend it if the regular method wins, even if you came in expecting to elect.

Book a Free Consultation