1. When freelance work forces registration

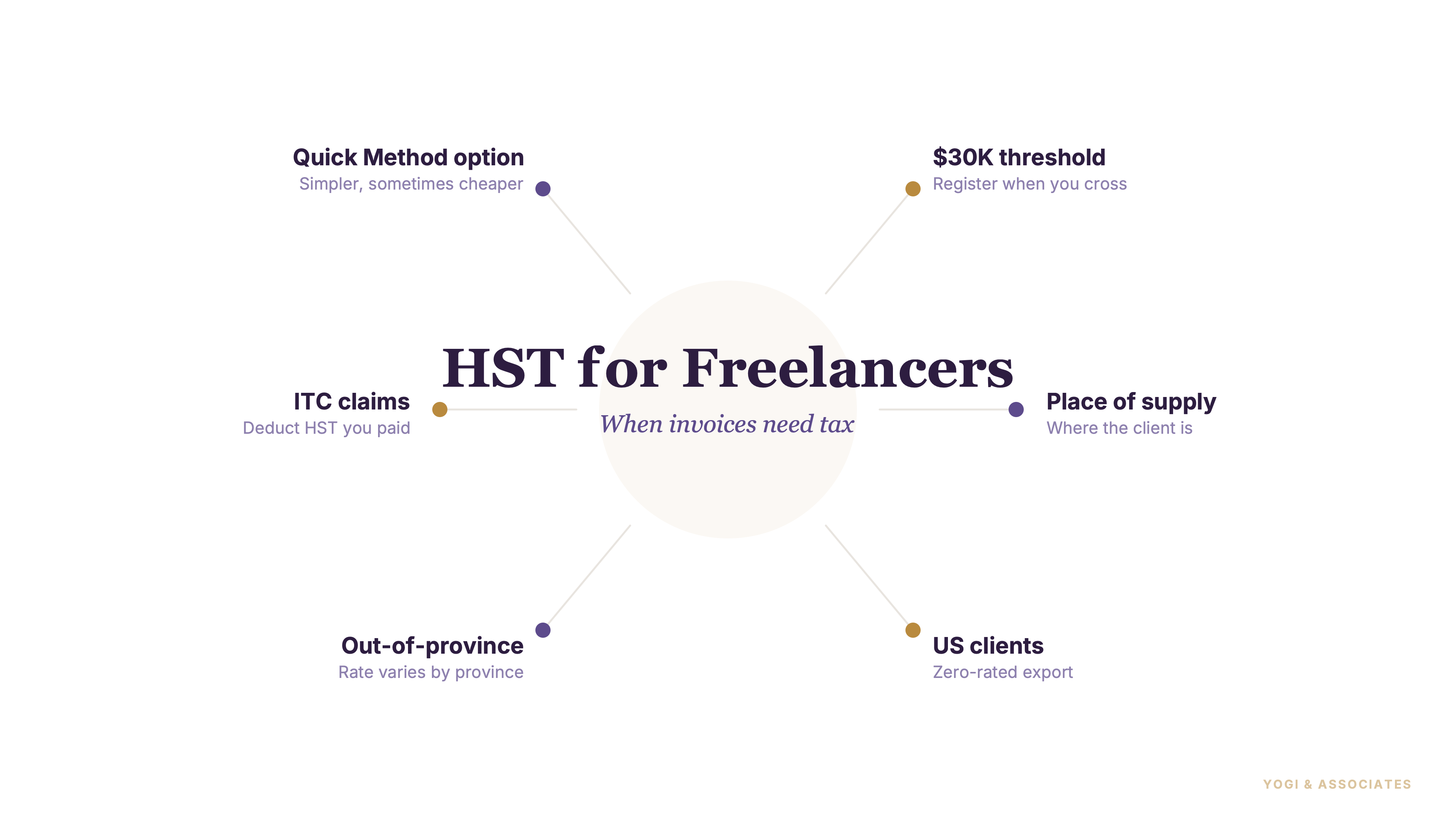

Freelancers don't get a special threshold. CRA uses the same $30,000 rule for self-employed people that it uses for every other small business.

Worldwide taxable revenues over four consecutive calendar quarters, or in any single calendar quarter, can trigger registration. This is where freelancers get caught: revenue rises quietly, the admin catches up months later, and the effective-date clock is already ticking.

If you're still below the line, track it monthly. Our GST/HST guide and our self-employed tax guide are the best starting pair for that stage.

2. Charging Canadian clients the right rate

The key concept is place of supply. That's CRA's term for where your sale is considered to happen, and for most services it tracks the client's province, not yours.

Here's the concrete test. Say you're a Toronto-based freelance designer billing three clients in the same month:

- Ontario client (Mississauga marketing agency): you charge 13% HST. Place of supply is Ontario.

- Manitoba client (Winnipeg SaaS startup): you charge 5% GST. Place of supply is Manitoba, a non-participating province, so only the federal portion applies.

- US client (a New York agency): you charge 0%. The service is zero-rated as an export to a non-resident.

One freelancer. One invoice template. Three different tax results. Your office address has no bearing on the rate — the client's location does. Getting this wrong is one of the fastest ways to charge the wrong tax on perfectly ordinary work, and it compounds quickly across a year of invoices.

3. Non-resident clients and zero-rating

A non-resident is someone whose normal place of business is outside Canada and who isn't registered for GST/HST here. Services made to a non-resident are often zero-rated — 0% tax charged, but the sale is still taxable for GST/HST purposes and you can still claim ITCs on related costs.

This isn't a free pass on every foreign invoice. CRA carves out exceptions: services related to real property in Canada, services performed mostly while the non-resident is physically in Canada, and services related to litigation in a Canadian court are not zero-rated. The service details still matter.

Freelancers oversimplify by saying all foreign clients are tax-free. That shortcut causes the most preventable trouble we see. If you want the registration side nailed down before invoicing goes out, read our GST/HST registration guide next.

4. ITCs freelancers usually care about

Once registered, freelancers care about ITCs fast. The usual list is boring but valuable: workspace costs, internet, phone, software, computer equipment, and vehicle expenses tied to client work.

CRA's rule is business use. Only the commercial-use portion is claimable — home office, phone, internet, and vehicle costs all need a real percentage behind them, not a vague “mostly for work.”

Capital property has an extra threshold. For a computer or similar equipment, more than 50% commercial use gets you the ITC; 50% or less wipes it out entirely. Our ITC guide goes deeper on the receipt rules and cutoffs.

5. Annual vs quarterly filing for freelancers

Most freelancers are nowhere near the reporting thresholds. CRA usually assigns annual filing because annual taxable supplies are under $1.5M.

Annual isn't always the right pick. Freelancers in a refund position during startup years often prefer quarterly because it recovers ITC money faster — waiting a full year for a refund on new laptop, software, and home-office costs ties up real cash.

The real question isn't workload. It's whether you usually owe or usually wait for a refund.

6. Instalments and cash-flow surprises

Annual filing sounds light until instalments show up. Annual filers with net tax of $3,000 or more in the previous fiscal year owe quarterly instalment payments.

That catches freelancers off guard because it feels like filing once should mean paying once. That one assumption causes more stress than the registration itself — especially when the first instalment notice arrives three months before the actual return is due.

If your freelance income jumped hard this year, don't wait for the reminder letter. Quarterly cash planning matters more than most freelancers expect.

7. Common freelancer HST mistakes

The usual errors are predictable. Not registering on time. Not charging GST/HST after crossing the threshold. Forgetting to include the registration number on invoices. Claiming personal expenses as if they were fully business costs.

Many freelancers also assume all foreign-facing work means no tax, even when the client is actually in Canada or the service doesn't fit the zero-rating rule. That mix of confidence and half-memory is where the real trouble starts.

If the file already feels messy, read our GST/HST mistakes guide before CRA reads it first. Cleaning it up early is almost always cheaper than defending it later.

Not sure if you're charging the right rate on your Alberta client, or whether your US work really is zero-rated? We review invoices, place-of-supply logic, and ITC percentages for GTA freelancers before the mistakes compound into a reassessment.

Book a Free Consultation