1. What EHT actually is

Ontario EHT is a provincial payroll tax. It is separate from the federal payroll deductions you already run through every pay cycle.

The province says the tax helps support OHIP. That matters because a lot of employers wrongly assume EHT is just another CRA remittance line, and it is not.

So if you already have payroll running and have only been watching federal deductions, add EHT to the same control list. In our view, that is the point where Ontario payroll starts feeling more real.

2. Who has to pay Ontario EHT

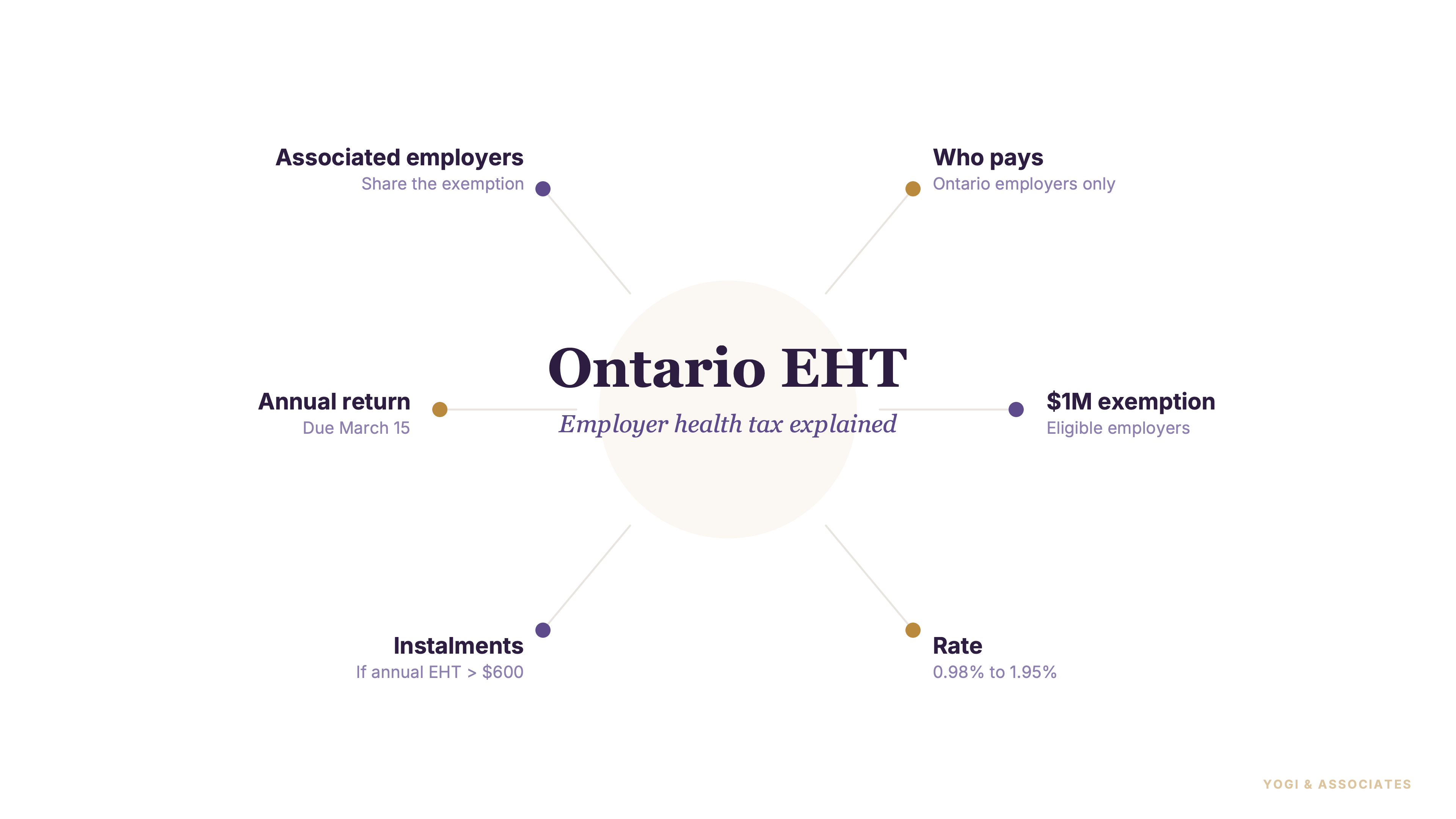

EHT generally applies when you are an employer with employees who report for work at an Ontario permanent establishment, or who are paid from one. That is the basic doorway into the tax.

Ontario remuneration (the total wages, salaries, bonuses, and taxable benefits paid to employees who work at an Ontario location) is the number the province cares about. This is where multi-province employers need to slow down, because the permanent-establishment detail matters.

So if payroll is already stretching, our Canadian payroll guide and our payroll service are the two starting points we would use. But the key point is simple: Ontario payroll can create Ontario EHT even if the federal payroll side is already under control.

3. The $1 million exemption is helpful, but limited

The headline number most small employers care about is the $1 million exemption. Eligible private-sector employers can generally avoid EHT on the first $1 million of Ontario remuneration.

But that is not universal. The province ties the exemption to eligible private-sector employers with annual Ontario remuneration of $5 million or less, and public-sector employers do not get it.

Owners hear "$1 million exemption" and stop reading too early. So the real checklist is: are you private-sector, are you under $5 million, and are you sharing the exemption with related companies.

4. The rate is a sliding scale, not one flat number

Ontario does not use one neat EHT rate for everyone. The rate starts at 0.98% on the smallest tier of remuneration and rises on a sliding scale to 1.95% once Ontario remuneration is above $400,000.

That matters because the exemption and the rate discussion are different conversations. Employers often blend them together and end up misunderstanding both.

Plus EHT sits beside the rest of payroll, not instead of it. So if you want the neighbouring federal deduction side refreshed, our CPP guide is the right next stop.

5. Associated employers do not get a free second exemption

This is the part that surprises growing groups. Associated employers (Ontario's term for related businesses that share owners — they must share the $1 million exemption between them, not get one each) cannot each claim the full exemption.

Ontario requires the associated group to share that $1 million across the group. This is one of the most important planning rules on the whole EHT file, because it kills the lazy assumption that each company gets a separate shelter.

So if you have sister companies, a holdco structure, or parent-subsidiary relationships, review the group before year-end. In our view, this is where good payroll advice saves real money.

6. Registration and filing deadlines matter

Ontario wants EHT registration done quickly. New employers are required to register within 15 days of first paying Ontario remuneration.

Registration can be done through ONT-TAXS Online, and Ontario also allows paper channels like mail or fax. The annual EHT return is due on or before March 15 of the following year.

This deadline gets lost because employers focus on February payroll slips first. So if you are building a proper year-end calendar, our year-end payroll checklist should sit right beside the EHT file.

7. Instalments and penalties are where pain starts

Once annual Ontario remuneration exceeds $1.2 million, monthly instalments can be required. Those instalments are generally due on the 15th day of each month.

Ontario also charges interest on overdue EHT. And if the annual return is late, a percentage-based penalty can apply on top of the tax owing.

This is the part employers should respect early, not later. So if EHT is starting to feel like one more moving piece that could go wrong, keep it tied to the same control process as your federal payroll remittances.

EHT gets more expensive when you notice it too late. If you want Ontario payroll set up cleanly before the threshold issues start, we can help.

Book a Free Consultation