1. Start with the core 2026 rates

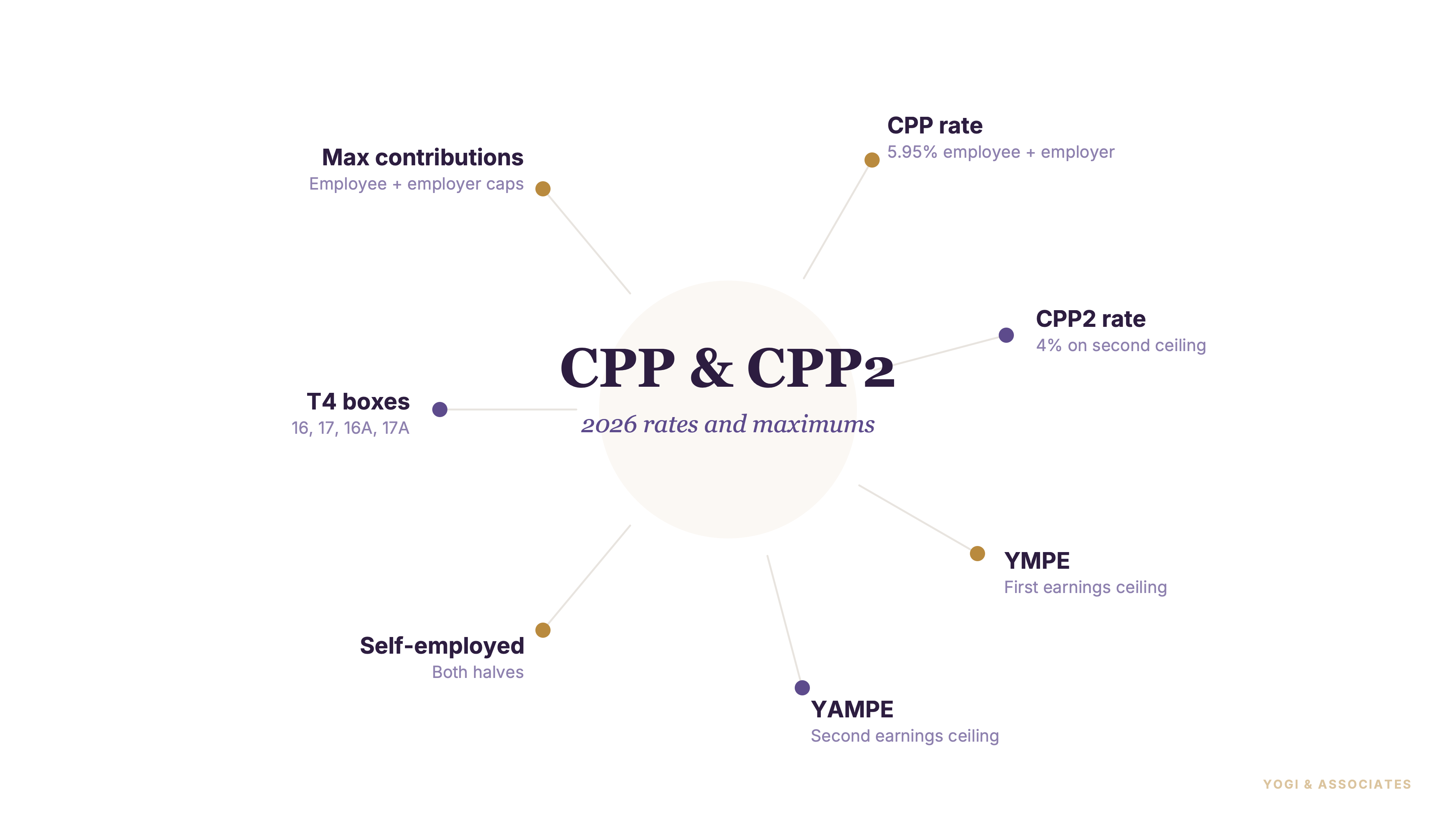

If you run payroll for an Ontario business, these are the CPP numbers you need for 2026. The base CPP contribution rate is 5.95% for employees and 5.95% for employers. That is still the main rate you will use on pensionable pay.

CPP2 sits on top of that, but only once earnings move above the first ceiling. This is the cleanest way to explain it: base CPP still handles the main band, and CPP2 only touches the upper band.

So if you want the broader rules around source deductions, start with our Canadian payroll guide. And if you want help actually running the numbers each pay cycle, our payroll service is built for exactly that.

2. Know the exemption, YMPE, and pensionable earnings

The 2026 basic exemption is $3,500. That means CPP does not apply to the first $3,500 of annual pensionable earnings.

After that, base CPP runs until the YMPE (Year's Maximum Pensionable Earnings — the salary cap above which base CPP stops being deducted), which is $74,600 for 2026. Pensionable earnings (the part of an employee's pay that CPP contributions are calculated on, after the basic exemption is removed) is the number you care about, not just gross pay.

This is where many employers get sloppy. So they see $74,600 and forget the $3,500 exemption is still part of the math before the maximum is reached.

3. Understand what CPP2 adds

CPP2 is the second layer that applies above the YMPE. For 2026, the YAMPE (Year's Additional Maximum Pensionable Earnings — the higher cap, ~14% above YMPE, that bounds the new CPP2 contribution) is $85,000.

So the CPP2 band for 2026 runs from $74,600 to $85,000. CRA says that if you earn between $74,600 and $85,000, you will make CPP2 contributions on $10,400.

The employee and employer CPP2 rate is 4.00% on that band. In our view, the easiest mistake to avoid is treating CPP2 like a totally separate payroll program. It is really just the upper slice of the same CPP story.

4. Know the 2026 maximum contributions

The maximum 2026 base CPP contribution is $4,230.45 for the employee and $4,230.45 for the employer. Once that base maximum is reached, base CPP stops.

But that does not always mean all CPP deductions stop. If the employee's pay is still inside the CPP2 band, the maximum CPP2 contribution is $416.00 for the employee and $416.00 for the employer.

This is the number set payroll teams should keep on one page: $4,230.45, $4,230.45, $416.00, and $416.00. Plus if an employee works for more than one employer, each employer still calculates CPP based on that employment alone.

5. Self-employed people pay both sides

If you are self-employed, you pay both the employee and employer halves of base CPP. That makes the 2026 self-employed base CPP rate 11.90%, with a maximum base contribution of $8,460.90.

And there is a CPP2 version of that rule too. The self-employed CPP2 rate is 8.00%, and the maximum self-employed CPP2 contribution is $832.00.

This catches new business owners off guard every year. So if you report business income on a T2125, read our self-employed tax guide as well, because CPP is one of the first costs that feels bigger once the income rises.

6. Put the right amounts in the right T4 boxes

On the T4, base CPP goes in box 16. CPP2 goes in box 16A. The pensionable earnings used to calculate those contributions go in box 26.

But do not mix those boxes up. CRA is very clear that CPP2 does not belong in box 16. This matters more now because box 16A is still new enough that some payroll files are being reviewed manually at year-end.

So if you are deciding how salary fits into the bigger owner-compensation picture, our salary vs dividends post is the next read. And if you need the filing calendar around T4 season, our 2026 tax deadlines guide lays it out.

7. Avoid the mistakes we see most often

The first mistake is using last year's thresholds. The second is forgetting that CPP2 starts only after the employee moves above $74,600 and stops at $85,000.

The third mistake is assuming a self-employed person only cares about the 11.90% base rate. In reality, once income pushes into the upper band, the 8.00% CPP2 rate matters too.

The safest approach is boring: update the payroll system early, test one employee file, and compare the T4 mapping before year-end. So if payroll has become a recurring headache, get help before the slips go out rather than after CRA spots a mismatch.

Want to see what a specific salary actually looks like once CPP, CPP2, EI, and tax come off? Plug the number into our Ontario payroll calculator — 2026 rates, employer’s side included.

CPP is easy to underestimate until payroll errors pile up. If you want the deductions, remittances, and T4 boxes handled cleanly, we can help.

Book a Free Consultation