1. The short version first

If you are saving for your first home in Ontario, the FHSA is the strongest registered account available to you right now. The selling point is simple: you get a deduction going in (like an RRSP) AND a tax-free qualifying withdrawal going out (like a TFSA). Both breaks, one account.

That's rare. It's why the FHSA usually moves to the top of the savings-stack conversation the moment a client qualifies.

Where FHSA fits in the stack — the Y&A default order for eligible first-time buyers:

- Employer RRSP match first, if you have one. Free money beats any tax break. Always capture the match before anything else.

- FHSA next, up to the $8,000 annual limit. The deduction-plus-tax-free-withdrawal combo is the strongest the Canadian system offers. Room only grows $8,000 a year and the account closes after 15 years, so you're time-gated on this one.

- TFSA for flexibility. For money you might actually need back for reasons other than a home purchase.

- Top up RRSP room if there's still saving capacity after the first three.

This is the starting point, not the final answer. Your income bracket, home timing, and spouse situation can all move the order. Our TFSA vs RRSP guide goes deeper on how to pick once FHSA room is maxed or unavailable.

2. Who can open an FHSA

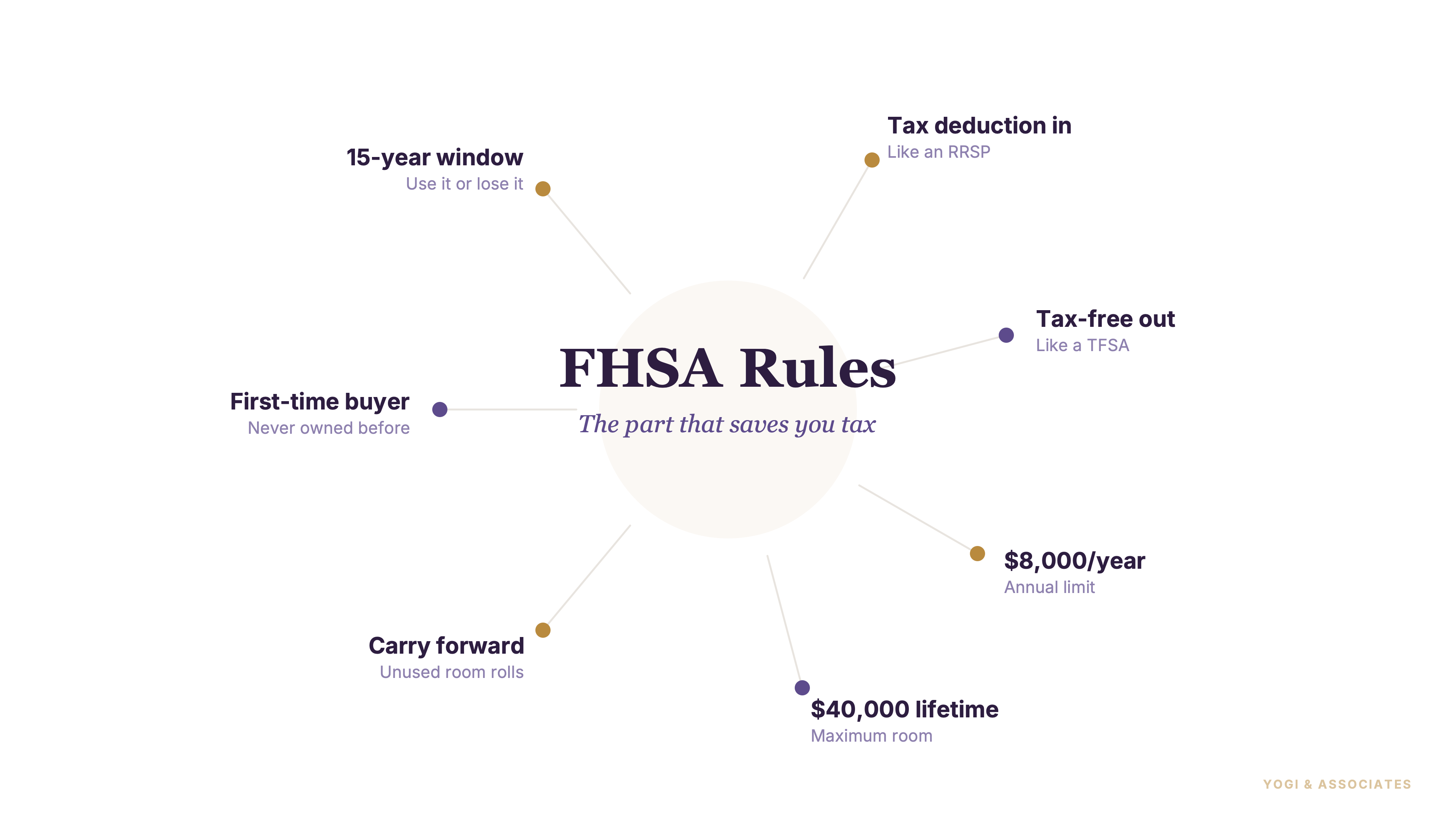

To open an FHSA, you need to be a qualifying individual. That means you are a resident of Canada, you are 18 or older, and you are 71 or younger as of December 31 of the year you open the account.

CRA also uses a first-time home buyer test. But the rule is stricter than many people expect: you must not have lived in a qualifying home that you owned or jointly owned in the current calendar year or the previous 4 calendar years.

The spouse rule is what people miss. You also cannot have lived in a qualifying home as your principal place of residence that your spouse or common-law partner owned or jointly owned in that same lookback period.

3. Contribution limits and carryforward room

The annual FHSA contribution limit is $8,000. The lifetime cap is $40,000.

Unused FHSA participation room carries forward, but only up to a maximum of $8,000. Missing one year doesn't automatically waste your room — but you can't stockpile it endlessly either. Skip too many years and the room tops out.

If you're trying to line up savings, home timing, and tax planning, our Canadian tax preparation guide is a good place to map the bigger picture.

4. How the tax benefits work

Contributions to an FHSA are generally deductible. A deduction reduces the income you pay tax on — so if you contribute $8,000 and you're in a 30% marginal bracket, your tax bill goes down by about $2,400 that year.

Qualifying withdrawals are tax-free. If you meet CRA's conditions and use the money for a qualifying first home, you don't bring that withdrawal into income at all.

Most registered accounts give you one break, not two. The FHSA gives you both: tax break going in, tax break coming out. That's the rare piece worth putting near the top of your savings priority list.

5. Withdrawals and the HBP

A qualifying withdrawal is the tax-free withdrawal that happens when you meet the FHSA rules for a qualifying home purchase. You can take that withdrawal in a single payment or a series of payments — you aren't locked into a one-shot drawdown.

You can also use the FHSA and the Home Buyers' Plan together on the same home. CRA allows you to withdraw from your RRSP under the HBP and make a qualifying withdrawal from your FHSA for the same qualifying home, as long as you meet the conditions for each.

This isn't an either-or choice. If you want help deciding how FHSA and HBP fit with your T1 and other savings choices, our personal tax service is where that planning usually gets cleaner.

6. If you do not buy a home

Not every FHSA ends with a purchase. But the account does not become useless if plans change.

CRA allows a direct transfer from your FHSA to your RRSP or RRIF without immediate tax consequences, as long as the transfer is direct and you do not have an excess FHSA amount. This takes a lot of pressure off people who are unsure about exact timing.

Or said another way, you are not forced into a taxable withdrawal just because the home purchase did not happen. Our tax filing deadlines guide is also useful once these transfers start showing up in your yearly filing flow.

7. When the account must close

The FHSA doesn't stay open forever. Your maximum participation period begins the day you open your first FHSA and ends on December 31 of the year when the earliest trigger happens.

Those triggers are: the 15th anniversary of opening your first FHSA, the year you turn 71, and the year following your first qualifying withdrawal. That deadline matters even if you still like the account and still have money in it — the clock runs regardless of how well things are going.

Don't leave this to the last minute. If the home purchase is off the table, plan the RRSP or RRIF transfer before the deadline shows up and forces a messier outcome.

8. How to open one — three steps

If this account is right for you, the mechanics are simpler than most Canadians expect. Here's the whole thing.

- Open the account at a bank, credit union, or brokerage. Pick one that lets you actually invest — not just a savings account paying 2%. An FHSA is only as useful as what's inside it. A cash FHSA earning 2% is a waste of the tax break.

- Contribute up to $8,000 for the year. Set up an auto-transfer on January 1 and forget it. most first-time buyers lose the room by forgetting to contribute — not by going over. And watch the ceiling: FHSA over-contributions get hit with a 1% per month tax on the excess, and unlike an RRSP, there's no $2,000 buffer. Every dollar over the line triggers the penalty.

- Withdraw for your qualifying home purchase. When the deal closes, your lawyer will ask for the purchase agreement. That's the document that unlocks the tax-free withdrawal. Fill out CRA Form RC725 (Request to Make a Qualifying Withdrawal from your FHSA), hand it to your FHSA issuer, and the money comes out clean.

Not sure which step you're on? That's where our personal tax service usually gets called in — we help GTA first-time buyers plan the contribution year and the withdrawal year together so nothing slips.

Frequently asked

Can I hold both an FHSA and a TFSA at the same time?

Yes. They're separate accounts with separate rules. Most first-time buyers we work with run both — FHSA for the home goal, TFSA for everything else. There's no rule that makes you pick.

Can I transfer money from my RRSP into an FHSA?

Yes. CRA allows a direct transfer from your RRSP into your FHSA using Form RC720. But the transfer uses up your FHSA contribution room, and it doesn't give you a second deduction — you already claimed one when the money went into the RRSP. And worth knowing: the transfer doesn't restore your RRSP room either. It's a way to reallocate, not a second tax break.

What if my spouse also contributes to their own FHSA?

Each spouse has their own $8,000 annual and $40,000 lifetime room. A couple can stack $80,000 tax-free toward the same first home. That's the biggest number most GTA first-time buyers hear all year.

Can I use the FHSA for a rental property or a second home?

No. Qualifying withdrawals are only for a home you'll live in as your principal residence within a year of buying or building it. Investment properties and cottages don't qualify. If any condition is missed, the issuer reports the withdrawal on a T4FHSA slip and the full amount lands on Line 12905 of your T1 as taxable income.

Is the $8,000 limit a calendar year or 12 rolling months?

Calendar year. January 1 to December 31. Miss December and you don't get a grace period — you lean on the carry-forward rule instead, and carry-forward caps at $8,000 at any point.

If I don't contribute this year, do I lose the room?

Not entirely. Unused FHSA participation room carries forward, but only up to a maximum of $8,000 at any one time. So skipping one year is fine. Skip three in a row and the room stops growing.

Not sure if FHSA should be your next dollar before RRSP or TFSA? We help GTA first-time buyers sort out contribution timing, spouse rules, and withdrawal planning before money goes to the wrong account.

Book a Free Consultation