1. Start with the 2026 EI rates

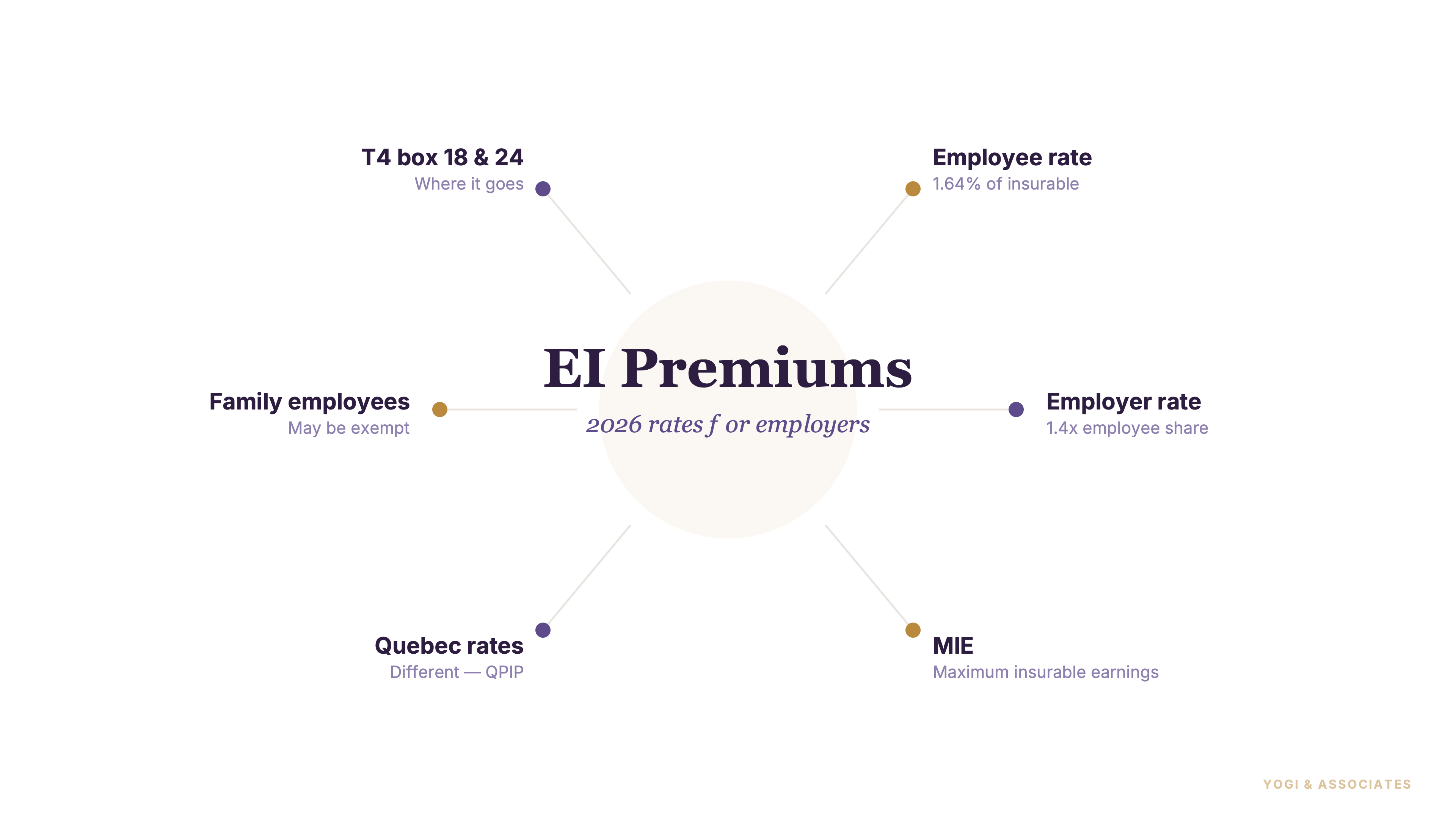

Ontario employers need these numbers every pay run. For 2026, the employee EI premium rate is $1.63 per $100 of insurable earnings. The employer rate is $2.28 per $100, because employers pay 1.4 times the employee rate.

That 1.4 times rule matters more than people think. Owners often remember the employee deduction and forget the employer share is bigger.

So if you want the full payroll picture beyond EI alone, start with our Canadian payroll guide. And if you need someone to run the deductions cleanly every pay cycle, our payroll service handles that work every day.

2. Know the MIE and annual maximums

The 2026 MIE (Maximum Insurable Earnings — the salary cap above which EI premiums stop being deducted for the year) is $68,900. Once an employee hits that ceiling, EI deductions stop for the rest of that year with that employer.

The maximum annual employee EI premium for 2026 is $1,123.07. The maximum annual employer EI premium for 2026 is $1,572.30.

This is the easiest payroll deduction to explain to staff. But it still gets mixed up with CPP, so it helps to compare it with our CPP and CPP2 guide for 2026 when someone is trying to read a pay stub properly.

3. Quebec has a different EI rate

Quebec does not use the same federal EI rate as the rest of Canada. For 2026, the Quebec employee EI rate is $1.30 per $100 of insurable earnings, and the Quebec employer rate is $1.82 per $100.

The reason is QPIP (Quebec Parental Insurance Plan — Quebec's separate program that replaces the federal EI parental benefit, which is why Quebec employees pay a lower federal EI rate). So Quebec payroll still has EI, just at a lower federal rate.

In our view, this is one of those payroll details that looks small until the wrong province setting sits in the file for months. And once that happens, cleanup is annoying fast.

4. Self-employed EI is opt-in, not automatic

Self-employed people do not pay EI automatically the way employees do. They can choose to opt into EI special benefits by registering with Service Canada.

That means maternity, parental, sickness, and other special benefits are possible, but only if the person has actually signed up. Many owners assume EI is built into self-employment by default, and it simply is not.

So if you report business income on a T2125, read our self-employed tax guide alongside this post. But do not assume self-employed EI works like regular payroll deductions.

5. Family employees are the biggest trap

This is where small businesses get burned. Non-arm's length (a tax term for related people — spouse, kids, parents, siblings — different rules apply to their employment) employment is generally not insurable for EI.

CRA says the exception is when the employer would have entered into a substantially similar contract with an arm's-length worker. And either the worker or the employer can ask CRA for a ruling on insurability.

Owners should never guess here. So if you are paying family through the business, read our guide on paying family members and get the EI side right before the slips go out.

6. Some work is outside the normal EI pattern

EI is not universal in the clean, simple way people assume. CRA says some employment may not be insurable, including related-party work that fails the arm's-length test and employment where the worker controls more than 40% of the voting shares of the corporation.

CRA also points to special EI rules for fishers, barbers, hairdressers, taxi drivers, and drivers of other passenger-carrying vehicles. The safest reading is this: if the work looks unusual, do not force it into a normal payroll template.

But the mistake we see most often is not the rare rule itself. It is acting certain before checking whether the employment is actually insurable.

7. Put EI in the right T4 boxes

On the T4, employee EI premiums go in box 18. Insurable earnings used to calculate those premiums go in box 24.

Those two boxes have to line up with the payroll history. This is one of the easiest year-end checks to do, and one of the dumbest places to make a preventable filing error.

So review the T4 mapping before filing, not after. And if year-end payroll keeps turning into cleanup work, get help before filing season rather than after CRA asks questions.

Curious what these EI numbers look like on a real paycheque? Run a salary through the Ontario payroll calculator — 2026 EI, CPP, CPP2, and tax on one screen, employer cost included.

EI is straightforward until one exception lands in the file. If you want payroll deductions and T4s handled properly, we can help.

Book a Free Consultation