1. Start with RC4110, not guesses

Ontario small businesses hire contractors constantly, and most of them skip the one step that actually matters. CRA's main guide on this issue is RC4110. If you are trying to decide worker status without it, you are basically making it up.

RC4110 asks the core question in plain terms: is the person working as an employee, or as someone in business on their own account. That wording matters, because it forces you to look past the invoice and into the relationship itself.

So before you build a hiring process around contractor labels, read the payroll basics in our Canadian payroll guide. And if the person really is carrying on an independent business, our self-employed tax guide shows what that life actually looks like on the tax side.

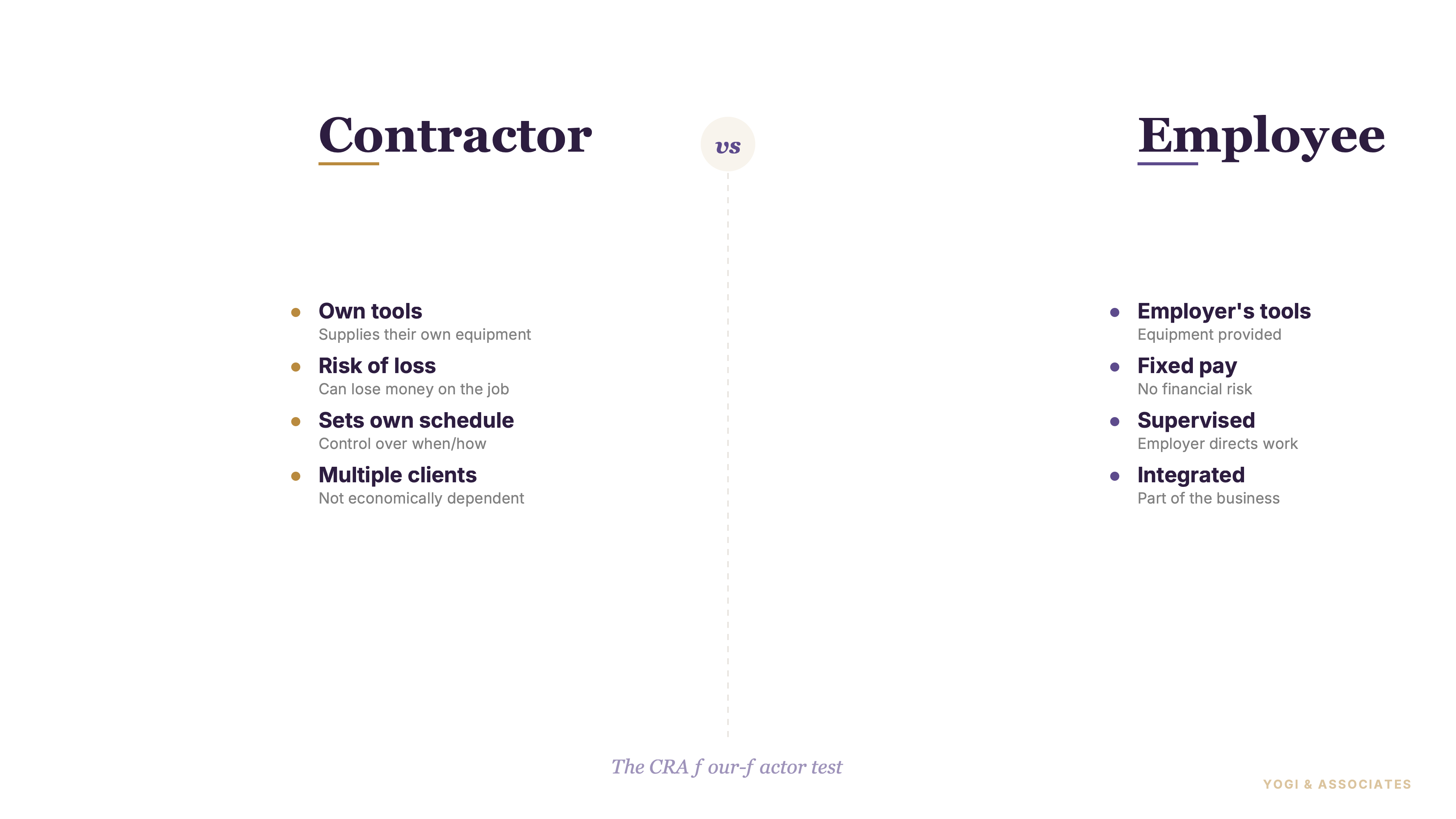

2. CRA looks at four factors together

CRA does not use a one-question shortcut. It looks at control, ownership of tools and equipment, chance of profit and risk of loss, and integration.

Control asks who decides how, when, and where the work is done. Tools asks who brings the meaningful equipment.

Profit and loss asks whether the worker can actually make more by working smarter, and whether they can actually lose money. Integration asks whether the worker is part of the payer's business or running a separate one.

Businesses get in trouble when they cherry-pick one factor. But CRA looks at the whole picture, not the nicest fact in your file.

3. Intent matters, but reality matters more

CRA does consider what both sides intended. If the contract says independent contractor, that is still part of the story.

But the guide says intent has to match the actual working relationship. So if the paper says contractor but the payer controls the hours, supplies the tools, pays an hourly amount, and folds the worker into the team, the paper will not save you.

In our view, this is the single biggest misunderstanding on the whole topic. And it is why a nicely drafted contractor agreement can still collapse under a routine CRA review.

4. The usual red flags are not subtle

CRA's examples and guidance point in the same direction over and over. A worker looks more employee-like when the payer controls the work, the payer provides the tools, the worker has little real chance of profit or loss, and the worker looks like part of the payer's business.

So the common problem case is not mysterious. It is the long-running "contractor" who works mainly for one payer, gets paid like staff, uses the payer's tools, has no business presence, and does not really carry business risk. Those files should make owners nervous immediately.

Plus the opposite is true too. A real contractor usually looks more like an independent business, not just an employee with an invoice template.

5. Misclassification gets expensive fast

If CRA decides the worker was really an employee, the payer can get hit hard. CRA says employers are responsible for deducting CPP, EI, and income tax from amounts paid to employees.

And if the payer failed to deduct the required CPP contributions or EI premiums, CRA says the payer has to pay both the employer's share and the employee's share, plus penalties and interest. But the problem usually does not stop there, because payroll income tax may also have been missed.

This is why classification should be treated as a payroll risk, not just a contract drafting issue. So if you want a sense of what can get back-charged, our CPP guide and our EI guide show the deduction systems you are stepping into.

6. Use CPT1 when the facts are muddy

CRA gives both sides a way to stop guessing. CPT1 (the CRA form either party can submit to request a binding ruling on whether work is pensionable and insurable) is the form used to ask CRA for a ruling.

Either the worker or the payer can request that ruling, and CRA says it should be sent to the appropriate CRA tax office. That is the right move when the facts are mixed and the relationship is going to matter for CPP or EI.

But do it early. In our view, a ruling before a dispute is a lot cheaper than an assessment after several years of payments.

7. Make the call before money starts flowing

The best time to decide classification is before the first payment, not after six months of habit. Once money is flowing the wrong way, every extra month makes cleanup worse.

So ask the boring questions early: who controls the work, who owns the tools, who carries business risk, and who has clients besides you. That short conversation is worth more than a fancy agreement signed too late.

And if you already know the worker should be on payroll, do not pretend otherwise just to keep admin light. In our view, clean payroll is almost always cheaper than messy reclassification.

Worker classification problems are cheap to prevent and ugly to unwind. If you want help setting up payroll the right way from day one, we can help.

Book a Free Consultation