1. What the two methods actually mean

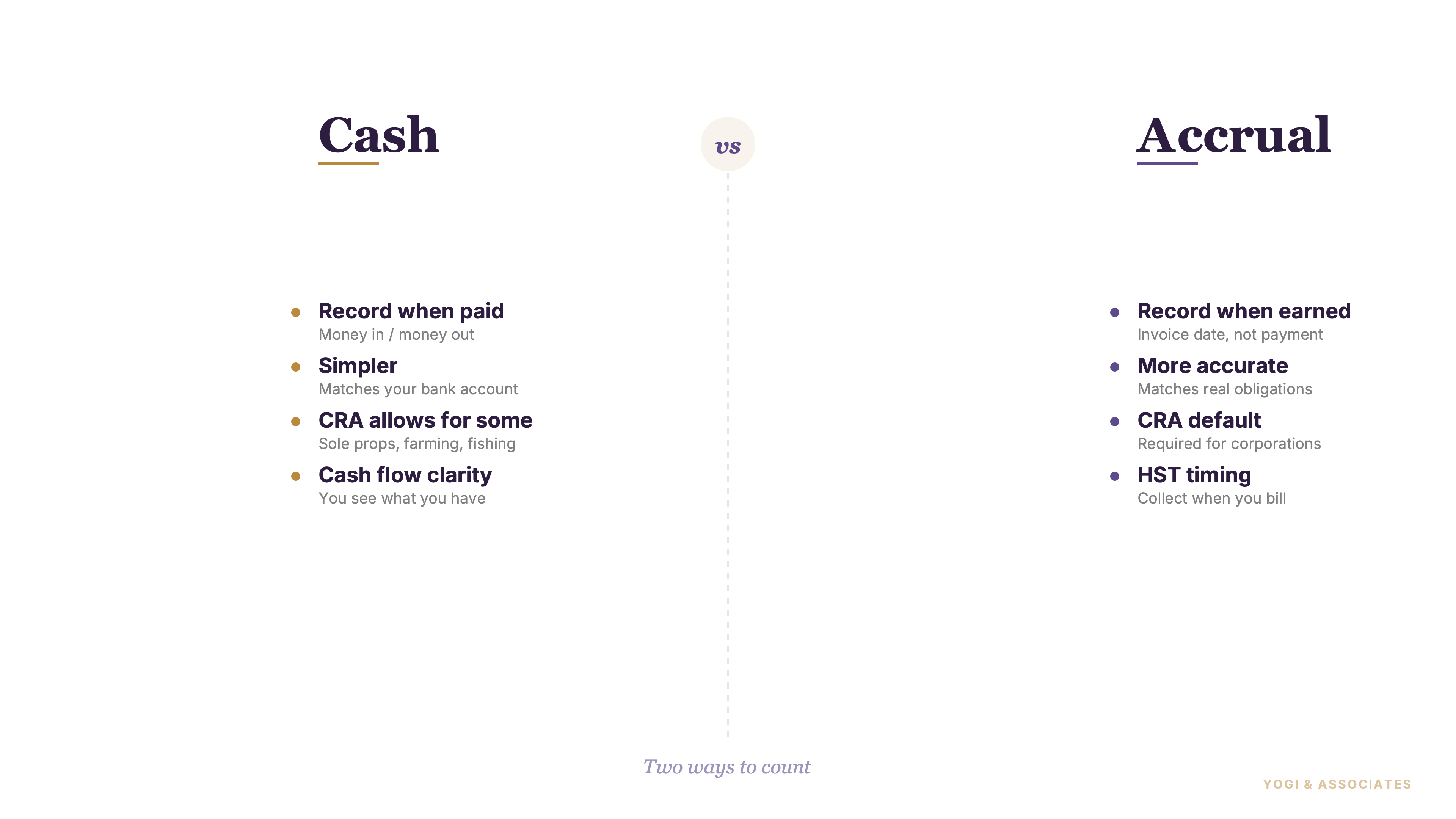

Cash basis follows the bank more closely. You record the sale when the money shows up, and you record the expense when the money leaves.

Accrual is different. And it cares about when the work was earned or the cost was incurred, even if cash has not moved yet.

This is the cleanest way to explain it to owners: cash tells you what hit the account, while accrual tells you what actually happened. that difference gets big fast once you start issuing invoices and carrying accounts receivable (money customers owe you for invoices you've issued but haven't been paid yet).

2. What CRA actually allows

CRA's general rule is not very flexible. It says business income generally has to be reported using the accrual method of accounting.

But there are specific exceptions. So the right question is not “which method do I prefer?” but “am I in one of the groups CRA lets choose?”

This is where a lot of bad advice starts. Our bookkeeping guide is the broader map, but the short version is simple: most businesses do not get a free choice here.

3. Who can still use cash basis

CRA says farmers, fishers, and self-employed commission agents can use the cash method or the accrual method to report income. All other self-employment income must be reported using the accrual method.

There is another catch inside that exception. The thing is, CRA also says farming activities can use the cash method, but separate business activities or GST/HST still have to follow accrual rules.

this is why owners should not assume one allowed exception changes everything. We've found the cash-method groups are narrower than people expect once mixed activities and HST are involved.

4. Why accrual usually tells the truth better

Accrual is more work, but it usually produces the better management view. It shows open invoices, unpaid bills, and timing mismatches that cash basis hides.

So a seasonal business can look fantastic on cash basis one month and weak the next, even when nothing important changed operationally. But accrual smooths that distortion because revenue and costs land closer to the work that created them.

That accuracy matters more than convenience for most established businesses. Our QuickBooks setup guide matters here too, because modern bookkeeping software can show either reporting view even when the underlying file is managed properly.

5. HST changes the conversation

HST is where many owners realize cash thinking is not enough. CRA says you must remit the GST/HST for any invoice you include in your return, even if you have not yet been paid.

CRA also says you become liable for the GST/HST you charge on the day you receive payment or the day payment is due, whichever is earlier. And that is an accrual-style rule even when the owner mentally runs the business off the bank balance.

this is the biggest source of confusion between bookkeeping and tax. Our GST/HST guide helps if you want the filing side, and our Quick Method article matters too because the Quick Method changes the remittance calculation, not the basic income-tax accounting method.

6. What happens if you switch methods

Switching is not just a setting change. If you are in one of the groups CRA lets use cash, CRA says you file the next return using the new method and attach a statement showing the income and expense adjustments caused by the change.

So the real issue is transition. Plus the adjustment exists to stop income or expenses from being counted twice, or missed entirely, when you move between methods.

This is where owners should slow down and get help. The thing is, the bookkeeping file, the tax return, and the HST timing all have to move together.

7. What most owners should do

Most Canadian business owners should expect accrual to be their long-term answer. It matches CRA's general rule, handles invoices and bills properly, and makes year-end reporting cleaner.

But cash basis can still be useful as a management lens. So we often look at both views internally, even when the formal reporting answer is accrual.

The best setup is simple: keep books clean enough for accrual, then use cash-style views to watch liquidity when needed. If the file is already messy, our bookkeeping service is usually the faster fix than trying to patch the method choice after the damage is done.

Cash and accrual sound simple until CRA, HST, and year-end adjustments get involved. If you want the method and bookkeeping cleaned up properly, we can help.

Book a Free Consultation